Coalition found that both claims frequency and severity rose for businesses in early 2023 across all revenue bands. Companies with over $100 million in revenue saw the largest increase (20%) in the number of claims as well as more substantial losses from attacks – with a 72% increase in claims severity from 2H 2022.

“The cyber threat landscape has become more volatile, and, as a result, we’ve seen claims become more severe and more common than ever,” said Chris Hendricks, Head of Coalition Incident Response.

“To help prevent these costly and disruptive incidents, organizations need to take an active role in improving their security defenses and make risk management a top priority,” added Hendricks.

Coalition’s report also saw a resounding increase in ransomware claims frequency in 1H 2023, which grew by 27% from 2H 2022. Claims severity also reached a record high, increasing 61% from the previous half and 117% over last year.

Moreover, cybercriminals increased their demands: the average ransom demand was $1.62 million, a 47% increase over the previous six months and a 74% increase over the past year.

Email security remained critical to claims reduction

The company also recovered an unprecedented $23 million in stolen funds — all of which went directly back to policyholders. Notably, Coalition’s total FTF (funds transfer fraud) recovery amount was nearly three times greater than 2H 2022. The average recovery amount was $612,000 per FTF claim, representing 79% of all FTF losses in instances where recovery was possible.

FTF claims frequency increased by 15% in 1H 2023, and FTF severity increased by 39% to an average loss of more than $297,000. This half, Coalition negotiated ransomware payments down to an average of 44% of the initial amount demanded.

Businesses using Google Workspace for email were markedly more secure than those using Microsoft Office 365 (M365) and on-premises Microsoft Exchange. M365 users were more than twice as likely to experience a claim compared to Google Workspace users. On-premises Microsoft Exchange users were nearly three times more likely to experience a claim than businesses using Google Workspace.

Overall, companies using Google Workspace experienced a 25% risk reduction for FTF or BEC claims and a 10% risk reduction for ransomware claims.

Security chiefs should shop early for coverage and prepare for long questionnaires about their companies’ cyber defenses, industry professionals say

Insurers are scrutinizing prospective clients’ cybersecurity practices more closely than in past years, when underwriting was less strict. PHOTO: GETTY IMAGES/ISTOCKPHOTO

For many businesses, obtaining or renewing cyber insurance has become expensive and arduous.

The price of cyber insurance has soared in the past year amid a rise in ransomware hacks and other cyberattacks. Given these realities, insurers are taking a harder line before renewing or granting new or additional coverage. They are asking for more in-depth information about companies’ cyber policies and procedures, and businesses that can’t satisfy this greater level of scrutiny could face higher premiums, be offered limited coverage or be refused coverage altogether, industry professionals said.

“Underwriting scrutiny has really tightened up over the past 18 months or so,” said Judith Selby, a partner in the New York office of Kennedys Law LLP.

In the second quarter, U.S. cyber-insurance prices increased 79% from a year earlier, after more than doubling in each of the preceding two quarters, according to the Global Insurance Market Index from professional-services firm Marsh & McLennan Cos.

Direct-written premiums for cyber coverage collected by the largest U.S. insurance carriers—the amounts insurers charge to clients, excluding premiums earned from acting as a reinsurer—climbed to $3.15 billion last year, up 92% from 2020, according to information submitted to the National Association of Insurance Commissioners, an industry watchdog, and compiled by ratings firms. Analysts attribute the increase primarily to higher rates, as opposed to insurers significantly expanding coverage limits.

Companies buying insurance are subject to tight scrutiny of internal cyber practices. This is different from past years, when carriers poured into the cyber market and competition produced less-stringent underwriting, Ms. Selby said.

Now, insurers aiming to limit their risk are putting corporate security chiefs through lengthy lists of questions about how they defend their companies, said Chris Castaldo, chief information security officer at Crossbeam Inc., a Philadelphia-based tech firm that helps companies find new business partners and customers.

“Prior to the questionnaires, you just gave them the coverage amount you wanted and the industry you were in, and that was it,” Mr. Castaldo said, referring to interactions with cyber insurers.

Discover Financial Services has a third party validate the robustness of its cybersecurity program, which helps with insurance, said CISO Shaun Khalfan. “Insurers want to have confidence that you are making the right investments and are building and maintaining a robust cybersecurity program,” Mr. Khalfan said.

Some of the questions insurers ask—and the level of detail required—can depend on the carrier, the size and type of the business seeking coverage and the amount of coverage desired.

Around 18 months ago, underwriters asked companies whether they required multifactor authentication when administrators accessed their system, said Tom Reagan, cyber practice leader in Marsh McLennan’s financial and professional products specialty practice. Today there’s an expectation that multifactor authentication is used throughout the organization, not just by administrators, he said.

Insurers also expect organizations to have planned and tested for a cyber event, such as through tabletop exercises, Mr. Reagan said: “They are not just interested in your smoke alarms, they want to hear about the fire drills.”

Carriers want to know what kind of backup plans companies have if a ransomware attack strikes and how those plans are tested. Insurers also diving deeper into whether a company’s networks are segregated to limit the spread of malware, Ms. Selby said. Other important criteria some insurers consider, she said, include endpoint protection, or monitoring and protecting devices against cyber threats, and incident-response exercises.

Some companies will need to work with more carriers than in the past to get the desired level of coverage because no single insurer wants to carry so much risk, Ms. Selby said.

Amid the changing landscape, Mr. Reagan recommended that companies start to re-evaluate their cyber-insurance needs as early as six months before a policy comes up for renewal. Starting earlier to identify possible holes allows businesses to make changes to their cyber defenses, if necessary, and gather information that carriers require, he said.

When security fails, cyber insurance can become crucial for ensuring continuity.

Cyber has changed everything around us – even the way we tackle geopolitical crisis and conflicts. When Einstein was asked what a war will look like in the future, he couldn’t have predicted the importance of digital technology for modern societies.

According to a report by IDC, by the end of 2022, nearly 65% of the global GDP will be digitized — reliant on a digital system of some kind. This shift to digital technology has created a new class of digital risks that are constantly evolving and strike faster and often with more severity than traditional risks. The events of the past two years have made this shift clear: from ransomware attacks to the challenges of managing distributed workforces, digital risk is different.

Our reliance on digital technology and the inherited risk is a key driving factor for buying cyber risk insurance. If the technology were to become unavailable, the resulting business impact could be mitigated with cyber insurance. Even if businesses invest in cybersecurity protections, as they increasingly do, security controls are not impenetrable. When security fails, cyber insurance can become crucial for ensuring continuity.

While traditional insurance has served mainly as a hedge against loss only after an incident, insurance designed for the digital economy needs to look at risk from a different angle, providing value before, during, and after an incident that could lead to a loss. This is essential for all businesses, as the analysis of security incidents that led to claims during 2021 reveals.

Ransom demands continue to increase. The ransomware business model has begun to mature, and the average ransom demand has increased by 20%.

The frequency of other attack techniques also rose as hackers expanded to new tactics. This heralds an era of omnidirectional threat. While ransomware may be the most newsworthy, no attack vector can be ignored.

Small businesses are disproportionately impacted. As attacks become increasingly automated, it has become easier and more profitable for criminals to target small organizations.

“We are noticing a drastic increase in both likelihood and severity of all types of cyber-attack,” says Isaac Guasch, cyber security specialist at Tokyo Marine HCC International. “Whether you are a small independent business or a large, international organization, the increasingly interconnected nature of the businesses that form our economies, is a key threat. Even if you are confident that your cyber security measures are up to date, those of your partners may not be, so you may need to constantly redefine your perimeter,” Guasch adds.

Evolving global risk environment alters the cyber insurancelandscape

However, not all risks are technology-related. Businesses operate in a hyper-connected environment where turbulences in one part of the world may have dire consequences in many remote markets. Geopolitical conflicts, societal upheavals, and financial cracks may put the stability of the business environment in question.

As digital technology and interconnectedness blur the boundaries with the physical world, it also becomes more difficult to calculate risk and set premiums. However, it is true that in times of global crisis, premiums do increase. For example, the Council of Insurance Agents & Brokers reported in March 2022 an average premium increase of 34.3% for cyber, marking the first time an increase of this magnitude is recorded since the events of 9/11.

As the global risk environment evolves and changes almost every day, the insurance industry needs to evolve as well. This level of evolution should not only cover cyber insurance but other forms of “traditional” insurance. For example, what happens if a facility is damaged or even destroyed because of a cybersecurity incident targeting a connected IoT device? What is the level of risk that each connected OT device exposes critical infrastructure to?

“With respect to insurance, cyber-attacks are not just affecting cyber liability policies. They are affecting many, if not all policies that are carried by a company,” Rick Toland, executive vice president at Waters Insurance Network, told Industrial Cyber. “Further, it is difficult to quantify where the cyber loss begins, and the property, automobile, GL, pollution or other policy begins and how the financial responsibility of each insurer will be allocated to pay the resulting loss,” Toland added.

Cyber insurance is not a panacea

Within a flux financial, technological, and geopolitical environment, many businesses, especially small-and-medium ones, tend to rely heavily on cyber insurers for answers to their cybersecurity posture challenges. However, buying cyber insurance cannot become the answer to all their security problems.

Instead, businesses can partner with an experienced managed security services company to guide and counsel them through the actions and best practices that can undertake now to better protect themselves against cyberthreats. Shaping a proactive and holistic cybersecurity strategy will better equip businesses in the event they need to submit a claim for losses or damages resulting from a ransomware attack or similar malicious activity.

Above all, it comes down to the basics. Organizations should start by analyzing the security controls they have in place to ensure adherence to guidelines developed by agencies like CISA, FBI, and ENISA, including multifactor authentication, employing antivirus and anti-malware scanning, enabling strong spam filters, updating software, and segmenting networks. Either way, failure to implement basic cyber hygiene measures is a no-go for buying cyber insurance.

About the author: Viral Trivedi

Viral Trivedi is the Chief Business Officer at Ampcus Cyber Inc—a pure-play cybersecurity service company headquartered in Chantilly, Virginia. As a CBO at Ampcus Cyber, Viral leads many customer-facing initiatives, including market strategy, channel partner programs, strategic accounts, and customer relationship management. He specializes in all aspects of managed security services, in both hands-on, and advisory roles. Viral has also held executive and senior management positions with small, and large organizations, and is also a Smart Cities & Critical Infrastructure Professional, as well as an active member of Infragard.

For these and other reasons, organizations are increasingly opting for cyber insurance coverage and paying higher premiums year after year. According to the U.S. Government Accountability Office, the number of companies opting for cybersecurity coverage grew from 26% in 2016 to 47% in 2020, and most saw breach insurance premiums increase by up to 30%.

Given the clear financial stakes, it is time security leaders understand the risks before adding cyber insurance to their strategy for ransomware prevention and recovery.

Successful breaches breed more attacks

Ransomware typically enters a company via a phishing attack or a compromise of a vulnerable system deployed on a network’s perimeter. From there, the infection proliferates via exploits or open shares, encrypting important data as it jumps from machine to machine, after which cyber criminals withhold the encryption key and threaten to publish sensitive data unless a ransom is paid.

The attackers, many of whom are part of sophisticated and organized groups, often provide a step-by-step guide for the targeted company to transfer ransoms in cryptocurrency, sometimes in the hundreds of thousands or millions of dollars. Sadly, when faced with costly downtime and/or the downstream effects of having sensitive data made public, many companies end up complying with the attackers’ demands. Paying the ransom, in turn, incentivizes more attacks, perpetuating the cycle of crime.

It’s important to note that cybersecurity insurance is also incentivizing attacks rather than serving as protection for the rarest of breaches. While U.S. law enforcement has typically urged companies not to pay the ransom, it has yet to decide to ban such payments altogether (though the US Department of the Treasury’s Office of Foreign Assets Control regulations prohibit U.S. companies from paying up if they suspect the attackers of being under its cyber-related sanctions program).

The limited availability of data on cyber incidents has made it difficult to develop full probabilistic models for use in pricing cyber insurance cover. While a few insurance companies, brokers and other companies have developed pricing models that provide quantifiable probabilistic estimates of potential losses based on Fair methodology, the vast majority of insurers still continue to use scenario-based approaches for estimating the potential frequency and severity of cyber incidents. Assessments of frequency and severity are usually based on publicly available data on past incidents. There are a few commercial companies that collect and market data on past incidents.

The insurability of a given risk is usually economically viable only where Risks must be quantifiable: the probability of occurrence of a given peril, its severity and its impact in terms of damages and losses must be assessable.

In the case of data confidentiality breaches, data on past breaches provides insurance companies with a basis to assess the level of risk based on different company characteristics and estimate the per record cost of a breach. Therefore, part of the underwriting process involves understanding the business activities and number and types of information records held by the company. Given the longer experience with data breach notification laws and the more developed stand-alone cyber insurance market, much of the available data is based on experience in the United States.

Insurance companies also focus significant attention on the company’s security practices and policies, depending on company size and amount of coverage being sought. For smaller companies/coverage amounts, the underwriting process will focus on basic cyber security practices such as use of a firewall, anti-virus/malware software and data encryption, as well as frequency of data backups and use of intrusion detection tools. In some cases, applications may ask about compliance with specific standards, such as the International Organization for Standardization standard on Information Security (ISO/IEC 27001); the US National Institute of Standards and Technology (NIST) Framework for Improving Critical Infrastructure Cybersecurity; or the UK Cyber Essentials. Companies that hold payment card information might also be asked about their compliance with the PCI Data Security Standard while US companies with health records might be asked about their compliance with Health Insurance Portability and Accountability Actsecurity requirements. Some stand-alone cyber insurance applications also request information on plans and policies, such as data protection policies, network access policies, internal auditing policies, disaster recovery plans, etc., as well as governance processes in place for those policies. Larger companies would face additional scrutiny, potentially involving on-site interviews, security audits and/or penetration testing. Risk and vulnerability assessments by external security consultants are offered by some companies as an additional service included as part of the insurance policy.

Insurance companies use the information gathered through the underwriting process to determine premium levels or deny the coverage. Some insurers may also establish minimum security standards that must be maintained through the coverage period in order for coverage to be maintained or sustained, such as timely patching of vulnerabilities and/or other software updates.

Cyber-insurance is an insurance product used to protect businesses and individual users from Internet-based risks, and more generally from risks relating to information technology infrastructure and activities. Cyber insurance purchased by an insured (first party) from an insurer (the second party) for protection against the claims of another (the third party). The first party is responsible for its own damages or losses whether caused by itself or the third party.

Cyber insurance may offer services products and countermeasures to protect business from known and unknown risks. There are now mandatory breach notification state laws (in many states) and regulation (HIPAA) which require breach notification. In services area cyber insurance may help organization to cover the cost of notifications and sometime may notify on behalf of an organization. The breach notification service may be necessary for SMB’s to acquire due to lack of necessary in-house resources. Depending on your business, few other items you may want to consider under cyber insurance are data restoration cost, payment of ransom, identity theft protection and reissuing of cards, potential downtime due to DDoS and potential regulatory fines.

How does a second party, an insurance company determine that first party premium (an amount to be paid for an insurance policy) and even decide that first party is insurable. The insurance company will look at organization’s security posture maturity based on industry standards and regulations (ISO, NIST, CSC, CSF) and determine if their Security Program is worthy of cyber insurance. Based on the existing security posture of an organization the second party will determine the risk they are willing to take and first party will determine the cost they are willing to pay for the premium. In the some cases insured might be able to absorb losses of the breach which were not covered by insurance but for some SMB’s these losses may be business limiting.

A point–in-time evaluation of an organization’s information security posture in constantly evolving, threat landscape only increases the challenge of insurance company to determine the first party premium. The insurance company may require a continuous feed to an organization security posture dash board which may also include but not limited to monitoring of security incident response on regular basis. Before making a decision on cyber insurance premium, an insurance company should utilize an in-house expertise or collaborate with InfoSec consulting organization to evaluate the frequency and severity of cyber threats facing an organization information security management system.

At end of the day, cyber insurance is a proactive security measure to counter potential data breaches and network security failures. Routinely, organizations are willing to spend money on security initiatives after the breach which is reactive action. Proactive security measures such as (developing sound security policies, compulsory cloud security, continuous monitoring, strong security awareness, effective BCP, proactive patching, resilient incident response plan…) may help not only to reduce the overall risk landscape but can assist in lowering the cyber insurance premium.

Proactive information security program which include but not limited to the basic cybersecurity measures may require acquiring cyber insurance. Insured organization (first party) may need to keep up with the basic cyber security measures to prevent voiding the coverage. When a functional and operational information security program which has a clear definition of an organization risk threshold becomes a priority, it can minimize potential risk of security breach and should be able to absorb losses for future security breach with cyber insurance as a part of risk management strategy.

DISC InfoSec assist in acquiring the cyber insurance which is aligned with business objectives and based on organization risk threshold. Before coverage is issued by the underwriter, in some cases, organization is asked to mitigate some risks to lower the premium. DISC InfoSec assist in compliance with standards, coverage inclusion/exclusion and risk mitigation process for organization acquiring cyber insurance.

Advancement of technology is deriving proliferation of threat landscape rapidly which extend attack vectors. With proliferation of automated tools available for cyber criminals; it’s not a matter of “if” but “when” there will be a security breach. There are two types of organizations in this category, those who’ve been hacked, and those who don’t know they have been hacked. The likelihood that your organization is next is not very unlikely. Is your organization prepared for a target of information security breach?

That will depend on if you have an operational Security Program which is functional enough to manage risk of a potential security breach. Now, the million-dollar question may be, is your Security Program resilient enough to sustain the risk and can it afford to absorb losses for future security breach. The security threats are evolving on daily basis and there are unknown threats like zero day threats where you need to add cyber insurance (which provides coverage from losses resulting from data breach or loss of confidential information) as a part of risk management strategy to tackle unnecessary disruptions to your business. As a part of risk management program, organizations regularly determine which risks to avoid, accept, control or transfer. This where transferring risk to cyber insurance take place and it can compensate for some residual risk.

Some may argue that they got liability insurance, which should cover security breach. Those days are behind us when organizations thought liability insurance were enough to cover the security breaches. Sony thought their general liability insurance covered them, but the court confirmed that policy did not have specific clauses to cover the security breach which was estimated $170M. Another highly publicized security breach of Target cost the retailer about $348M but the retailer had only $100M in cyber insurance coverage from multiple underwriters.

If you want a cyber liability policy, or want the lowest possible premiums, it is important to understand the security controls that most cyber underwriters expect to see. They will differ based on carrier, individual underwriter, organization size, industry, etc. and are subject to change.

The cyber insurance market continues to be marked by volatility, keeping insureds and underwriters alike on their toes.

In early 2021, the market shifted very abruptly, and increasing frequency, severity, and the sophistication of cybercrime pushed cyber underwriters to re-evaluate their approach to pricing, appetite, coverage, and underwriting.

Insureds renewing cyber insurance programs in the last 18 months know that underwriters have substantially upped their game when it comes to underwriting cyber risk.

At the beginning of this shift to a hard market, there was a definitive change to more detailed and technical underwriting. There was also inconsistency regarding the network security controls that were considered the most important, but today, the markets are in closer alignment.

Below are the top 10 network security controls that most cyber underwriters expect to see. They will differ based on carrier, individual underwriter, organization size, industry, etc. and are subject to change.

1) Comprehensive Multi-factor Authentication (MFA) plus Strong Password Controls

MFA (privileged access, remote access, remote cloud-based apps/O365) and strong password controls protect an organization against phishing, social engineering and password brute-force attacks and help prevent logins from attackers exploiting weak or stolen credentials. For many cyber underwriters, this is the most important control.

2) Network Segregation and Network Segmentation

Network segregation (separation of critical networks from the internet) and network segmentation (splitting larger networks into smaller segments) help reduce the risk and potential impact of ransomware attacks and will improve IT professionals’ auditing and alerting capabilities, which will assist in identifying cyber threats and responding to them.

3) Strong Data Backup Strategy

A strong data backup strategy is typically part of a solid disaster recovery/business continuity plan.

Underwriters want to see daily data backups, backups stored in more than one location, access rights limited to data backups, etc.

4) Disabled Administrative Privileges on Endpoints

Disabling administrative privileges on endpoints improves security posture. An administrative end-user on an endpoint for even a few minutes can lead to catastrophic data breaches if the endpoint is compromised.

5) Security Awareness Training for Employees

Security awareness has never been more important. The threat environment is evolving rapidly. Regular and frequent employee training is a must in today’s environment.

6) Endpoint Detection and Response (EDR) and Anti-Malware

EDR provides advanced measures for detecting threats and provides the ability to identify the origin of an attack as well as how it is spreading.

Anti-malware is a version of EDR — it scans your system for known malware such as trojans, worms, and ransomware, and upon detecting them, removes them. Underwriters look for both.

7) Sender Policy Framework (SPF)

SPF plays an important role in email authentication. It helps prevent emails from unauthorized senders from hitting an employee’s inbox. Underwriters look for this defensive tool.

8) 24/7 Security Operation Center (SOC)

A dedicated SOC acts as the first line of defense against cyber threats. The analysis and threat hunting conducted by SOC teams help prevent attacks from occurring in the first place.

SOCs provide increased visibility and control over security systems, enabling the organization to stay ahead of potential attackers. Cyber underwriters view this as a key proactive approach to network security.

9) Security Information Event Management (SIEM) Platform

SIEM tools collect and aggregate log and event data to help identify and track breaches.

They are powerful systems that provide security professionals with insight into what is happening in their IT environment and help track relevant events that have happened in the past.

10) Strong Service Accounts Security in Active Directory

Assigning service accounts in built-in privileged groups, such as the local Administrators or Domain Admins group, can be risky. Underwriters want service accounts removed from Domain Admin groups.

The implementation of these top 10 network security controls does not represent the full extent of the cyber underwriting process nor will they be the basis for a premium discount.

There are a host of additional controls, policies, procedures, and processes that underwriters will be evaluating. But checking these boxes will provide insureds with a solid foundation designed to meet the baseline expectations of cyber underwriters.

The cybersecurity insurance sector is experiencing swift expansion, with its value surging from around $13 billion in 2022 to a projected $84 billion by 2030, reflecting a robust 26% compound annual growth rate (CAGR). However, insurance providers are encountering challenges when it comes to accurately assessing the potential hazards associated with providing coverage for this category of risk.

Conventional actuarial models are ill-suited for an arena where exceptionally driven, innovative, and astute attackers are actively engaged in orchestrating events that lead to insurable incidents. Precisely gauging potential losses holds utmost importance in establishing customer premiums. However, despite a span of twenty years, there exists a substantial variance in loss ratios across insurance providers, ranging from a deficit of 0.5% to a surplus of 130.6%. The underwriting procedures lack the necessary robustness to effectively appraise these losses and set premiums that reflect a reasonable pricing.

Why is the insurance industry struggling with this?

The problem is with the nature of the threat. Cyber attackers escalate and adapt quickly, which undermines the historical-based models that insurance companies rely on. Attackers are continually shifting their maneuvers that identify victims, cause increasing loss, and rapidly shift to new areas of impact.

Denial of service attacks were once popular but were superseded by data breaches, which cause much more damage. Recently, attackers expanded their repertoire to include ransomware-style attacks that increased the insurable losses ever higher.

Trying to predict the cornerstone metrics for actuary modelers – the Annual Loss Expectancy and Annual Rate of Occurrence – with a high degree of accuracy is beyond the current capabilities of insurers. The industry currently conducts assessments for new clients to understand their cybersecurity posture to determine if they are insurable, what should be included/excluded from policies, and to calculate premiums. The current process is to weigh controls against best practices or peers to estimate the security posture of a policyholder.

However, these rudimentary practices are not delivering the necessary level of predictive accuracy.

The loss ratio for insurance firms has been volatile, in a world where getting the analysis wrong can be catastrophic. Variances and unpredictability make insurers nervous. At maximum, they want a 70% loss ratio to cover their payouts and expenses and, according to the National Association of Insurance Commissioners Report on the Cyber Insurance Market in 2021, nearly half of the top 20 insurers, representing 83% of the market, failed to achieve the desired loss ratio.

In response to failures to predict claims, insurers have been raising premiums to cover the risk gap. In Q4 2021 the renewals for premiums were up a staggering 34%. In Q4 2022 premiums continued to rise an additional 15%.

There are concerns that many customers will be priced out of the market and the insurance industry and left without a means of transferring risk. To the detriment of insurers, the companies may make their products so expensive that they undermine the tremendous market-growth opportunity. Additionally, upper limits for insurability and various exception clauses are being instituted, which diminish the overall value proposition for customers.

The next generation of cyber insurance

What is needed are better tools to predict cyber attacks and estimate losses. The current army of insurance actuaries has not delivered, but there is hope. It comes from the cyber risk community that looks to manage these ambiguous and chaotic risks by avoiding and minimizing losses.

These cybersecurity experts are motivated by optimizing limited resources to prevent or quickly undermine attacks. As part of that continuous exercise, there are opportunities to apply best practices to the insurance model to identify the most relevant aspects that include defensive postures (technology, behaviors, and processes) and understanding the relevant threat actors (targets, capabilities, and methods) to determine the residual risks.

The goal would be to develop a unified standard for qualifying for cyber insurance that would adapt to the rapid changes in the cyber landscape. More accurate methodologies will improve assessments to reduce insurers’ ambiguity so they may competitively price their offerings.

In the future, such calculations will be continuous and showcase how a company will benefit by properly managing security in alignment with shifting threats. This should bring down overall premium costs.

The next generation of cyber insurance will rise on the foundations of new risk analysis methodologies to be more accurate and sustain the mutual benefits offered by the insurance industry.

Are war exclusion clauses fit for purpose under International Humanitarian Law as cyber-attacks?

When UK and US said it was Russia, they weren’t thinking of the litigators!

Among the victims was US food giant Mondelez – the parent firm of Oreo cookies and Cadburys chocolate – which is now suing insurance company Zurich American for denying a £76m claim filed in October 2018, a year after the NotPetya attack. According to the firm, the malware rendered 1,700 of its servers and 24,000 of its laptops permanently dysfunctional.

In January, Zurich rejected the claim, simply referring to a single policy exclusion which does not cover “hostile or warlike action in time of peace or war” by “government or sovereign power; the military, naval, or air force; or agent or authority”.

On Thursday, trades handled by the world’s largest bank in the globe’s biggest market traversed Manhattan on a USB stick.

Industrial & Commercial Bank of China Ltd.’s U.S. unit had been hit by a cyberattack, rendering it unable to clear swathes of U.S. Treasury trades after entities responsible for settling the transactions swiftly disconnected from the stricken systems. That forced ICBC to send the required settlement details to those parties by a messenger carrying a thumb drive as the state-owned lender raced to limit the damage.

The workaround — described by market participants — followed the attack by suspected perpetrator Lockbit, a prolific criminal gang with ties to Russia that has also been linked to hits on Boeing Co., ION Trading U.K. and the U.K.’s Royal Mail. The strike caused immediate disruption as market-makers, brokerages and banks were forced to reroute trades, with many uncertain when access would resume.

The incident spotlights a danger that bank leaders concede keeps them up at night — the prospect of a cyber attack that could someday cripple a key piece of the financial system’s wiring, setting off a cascade of disruptions. Even brief episodes prompt bank leaders and their government overseers to call for more vigilance.

“This is a true shock to large banks around the world,” said Marcus Murray, the founder of Swedish cybersecurity firm Truesec. “The ICBC hack will make large banks around the globe race to improve their defenses, starting today.”

https://time.com/robots.txt?upapi=true

As details of the attack emerged, employees at the bank’s Beijing headquarters held urgent meetings with the lender’s U.S. division and notified regulators as they discussed next steps and assessed the impact, according to a person familiar with the matter. ICBC is considering seeking help from China’s Ministry of State Security in light of the risks of potential attack on other units, the person said.

Late Thursday, the bank confirmed it had experienced a ransomware attack a day earlier that disrupted some systems at its ICBC Financial Services unit. The company said it isolated the affected systems and that those at the bank’s head office and other overseas units weren’t impacted, nor was ICBC’s New York branch.

The extent of the disruption wasn’t immediately clear, though Treasury market participants reported liquidity was affected. The Securities Industry and Financial Markets Association, or Sifma, held calls with members about the matter Thursday.

ICBC FS offers fixed-income clearing, Treasuries repo lending and some equities securities lending. The unit had $23.5 billion of assets at the end of 2022, according to its most recent annual filing with U.S. regulators.

The attack is only the latest to snarl parts of the global financial system. Eight months ago, ION Trading U.K. — a little-known company that serves derivatives traders worldwide — was hit by a ransomware attack that paralyzed markets and forced trading shops that clear hundreds of billions of dollars of transactions a day to process deals manually. That has put financial institutions on high alert.

ICBC, the world’s largest lender by assets, has been improving its cybersecurity in recent months, highlighting increased challenges from potential attacks amid the expansion of online transactions, adoption of new technologies and open banking.

“The bank actively responded to new challenges of financial cybersecurity, adhered to the bottom line for production safety and deepened the intelligent transformation of operation and maintenance,” ICBC said in its interim report in September.

Ransomware attacks against Chinese firms appear rare in part because China has banned crypto-related transactions, according to Mattias Wåhlén, a threat intelligence specialist at Truesec. That makes it harder for victims to pay ransom, which is often demanded in cryptocurrency because that form of payment provides more anonymity.

But the latest attack likely exposes weaknesses in ICBC’s defenses, Wåhlén said.

“It appears ICBC has had a less effective security,” he said, “possibly because Chinese banks have not been tested as much as their Western counterparts in the past.”

Record levels

Ransomware hackers have become so prolific that attacks may hit record levels this year.

Blockchain analytics firm Chainalysis had recorded roughly $500 million of ransomware payments through the end of September, an increase of almost 50% from the same period a year earlier. Ransomware attacks surged 95% in the first three quarters of this year, compared with the same period in 2022, according to Corvus Insurance.

In 2020, the website of the New Zealand Stock Exchange was hit by a cyberattack that throttled traffic so severely that it couldn’t post critical market announcements, forcing the entire operation to shut down. It was later revealed that more than 100 banks, exchanges, insurers and other financial firms worldwide were targets of the same type of so-called DDoS attacks simultaneously.

Caesars Entertainment Inc., MGM Resorts International and Clorox Co. are among companies that have been hit by ransomware hackers in recent months.

ICBC was struck as the Securities and Exchange Commission works to reduce risks in the financial system with a raft of proposals that include mandating central clearing of all U.S. Treasuries. Central clearing platforms are intermediaries between buyers and sellers that assume responsibility for completing transactions and therefore prevent a default of one counterparty from causing widespread problems in the marketplace.

The incident underscores the benefits of central clearing in the $26 trillion market, said Stanford University finance professor Darrell Duffie.

“I view it as one example of why central clearing in the U.S. Treasuries market is a very good idea,” he said, “because had a similar problem occurred in a not-clearing firm, it’s not clear how the default risk that might result would propagate through the market.”

The threat actor who posted the data for sale has claimed credit for multiple other breaches, including one at grocery platform Weee! that exposed data on more than 1.1 million customers.

Hundreds of US lawmakers and their families are at risk of identity theft, financial scams, and potentially even physical threats after a known info-theft threat actor called IntelBroker made House of Representatives members’ personally identifiable information (PII) available for sale on the “Breached” criminal forum.

The information, confirmed as being obtained via a breach at health insurance marketplace DC Health Link, includes names, Social Security numbers, birth dates, addresses, and other sensitive identifying information. The data on the House members was part of a larger data set of PII belonging to more than 170,000 individuals enrolled with DC Health Link that the threat actor put up for sale this week.

DC Health Link: A Significant Breach

In a March 8 email to members of the House and their staff, US House Chief Administrative Officer Catherine Szpindor said the attack on DC Health Link does not appear to have specifically targeted US lawmakers. But the breach was significant and potentially exposed PII on thousands of people enrolled with DC Health Link.

“The FBI also informed us that they were able to purchase this PII, along with other enrollee information, on the Dark Web,” Speaker of the House Kevin McCarthy (R-Calif.) and House Minority Leader Hakeem Jeffries (D-N.Y.) said in a joint letter to the executive director at DC Health Link on March 8. The letter sought specifics from the health exchange on the breach, including details on the full scope of the attack and DC Health Link’s plans to notify affected individuals and offer credit monitoring services for them.

Despite the letter, details of the intrusion at DC Health Link are not yet available. The organization, governed by an executive board appointed by the DC mayor, did not immediately respond to a request for comment on the incident.

A report in BleepingComputer this week first identified the threat actor as the appropriately named IntelBroker, after the cybercriminals put the stolen data up for sale on March 6. According to the underground forum ad, the data set is available for “an undisclosed amount in Monero cryptocurrency.” Interested parties are asked to contact the sellers via a middleman for details.

IntelBroker’s Resume of Previous Breaches

This is not the first big heist for the group: A threat actor, using the same moniker in February, had claimed credit for a breach at Weee!, an Asian and Hispanic food delivery service. IntelBroker later leaked some 1.1 million unique email addresses and detailed information on over 11.3 million orders placed via the service.

Security vendor BitDefender, which covered the incident in its blog at the time, published an ad that IntelBroker placed on BreachedForums that showed the attacker boasting about obtaining full names, email addresses, phone number, and even order notes which included apartment and building access codes.

Meanwhile, Chris Strand, chief risk and compliance officer at Cybersixgill says his company has been tracking IntelBroker since 2022 and is about to release a report on the actor. “IntelBroker is a highly active Breached member with an 9/10 reputation score, who claimed in the past to be the developer of Endurance ransomware,” Strand says.

IntelBroker’s use of Breached to sell the health exchange PII, instead of a dedicated leak site or a Telegram channel, is consistent with the threat actor’s previous tactics. It suggests either a lack of resources or inexperience on the individual’s part, Strand says.

“In addition to IntelBroker’s presence on Breached, the threat actor has maintained a public GitHub repository titled Endurance-Wiper,” he tells Dark Reading.

In November, IntelBroker claimed that it used Endurance to steal data from high level US government agencies, Strand notes. The threat actor has in total made some 13 claims about breaching top US government agencies, likely to attract customers to a ransomware-as-a-service (RaaS) program. Other organizations that IntelBroker claims to have broken into include Volvo, cult footwear maker Dr. Martens, and an Indonesian subsidiary of The Body Shop.

“Our intelligence analysts have been tracking IntelBroker since 2022, and we have been collecting intel attributed to that threat actor since then, as well as associated threats that have been related or attributed to IntelBroker,” Strand says.

Is House Members’ PII a National Security Threat?

Justin Fier, senior vice president of red team operations at Darktrace, says the threat actor’s reason for putting the data up for sale appears to be purely financially motivated rather than political. And given the high profile of the victims, IntelBroker may find that the attention the breach is garnering will increase the value of the stolen data (or bring more heat than it would like).

The buyers might be another story. Given the availability of physical addresses and electronic contact information, the kinds of potential follow-on attacks are myriad, ranging from social engineering for identity theft or espionage, to physical targeting, meaning that interested parties could run the gamut in terms of motivation.

“The amount tells you a great deal about who they may be thinking of in terms of buyers,” he says. If all that the threat actor ends up asking is a couple of thousand dollars, they are likely to be a smaller criminal enterprise. But “you start talking millions, they are clearly then catering to nation-state buyers,” he says.

Fier assesses that the data that the threat actor stole on US House members as potentially posing a national security issue. “We shouldn’t only think external nation-states that might want to purchase this,” Fier says. “Who is to say that other political parties and/or activists couldn’t weaponize it?”

A survey of cybersecurity decision makers found 77 percent think the world is now in a perpetual state of cyberwarfare.

In addition, 82 percent believe geopolitics and cybersecurity are “intrinsically linked,” and two-thirds of polled organizations reported changing their security posture in response to the Russian invasion of Ukraine.

Of those asked, 64 percent believe they may have already been the target of a nation-state-directed cyberattack. Unfortunately, 63 percent of surveyed security leaders also believe that they’d never even know if a nation-state level actor pwned them.

The survey, organized by security shop Venafi, questioned 1,100 security leaders. Kevin Bocek, VP of security strategy and threat intelligence, said the results show cyberwarfare is here, and that it’s completely different to many would have imagined. “Any business can be damaged by nation-states,” he added.

According to Bocek, it’s been common knowledge for some time that government-backed advanced persistent threat (APT) crews are being used to further online geopolitical goals. Unlike conventional warfare, Bocek said, everyone is a target and there’s no military or government method for protecting everyone.

Nor is there going to be much financial redress available. Earlier this week Lloyd’s of London announced it would no longer recompense policy holders for certain nation-state attacks.

Late on Friday, Facebook agreed in principle to settle a US lawsuit seeking damages for letting third parties, including Cambridge Analytica, access the private data of users. The terms of the settlement have yet to be finalized.

Googlers uncover Charming email scraping tool

Researchers at Google’s Threat Analysis Group (TAG) have detailed email-stealing malware believed to be from Iranian APT Charming Kitten.

The tool, which TAG has dubbed Hyperscrape, is designed to siphon information from Gmail, Yahoo! and Outlook accounts. Hyperscrape runs locally on the infected Windows machine, and is able to iterate through the contents of a targeted inbox and individually download messages. To hide its tracks, it can, among other things, delete emails alerting users to possible intrusions.

Not to be confused with Rocket Kitten, another APT believed to be backed by Iran, Charming Kitten has been hijacking accounts, deploying malware, and using “novel techniques to conduct espionage aligned with the interests of the Iranian government” for years, TAG said.

In the case of Hyperscrape, it appears the tool is either rarely used, or still being worked on, as Google said it’s only seen fewer than two dozen instances of the software nasty, all located within Iran.

The malware is limited in terms of its ability to operate, too: it has to be installed locally on a victim’s machine and has dependencies that, if moved from its folder, will break its functionality. Additionally, Hyperscrape “requires the victim’s account credentials to run using a valid, authenticated user session the attacker has hijacked, or credentials the attacker has already acquired,” Google said.

While its use may be rare and its design somewhat restrictive, Hyperscrape is still dangerous malware that Google said it has written about to raise awareness. “We hope doing so will improve understanding of tactics and techniques that will enhance threat hunting capabilities and lead to stronger protections across the industry,” Google security engineer Ajax Bash wrote.

Security professionals can find the indicators of compromise data for Hyperscrape in Google’s report.

French agency may investigate Google – again

A French governmental agency that has twicefined Google over violations of data privacy regulations and the GDPR has been tipped off by the European Center for Digital Rights (NOYB) about another potential bad practice: dressing up adverts to look like normal email messages.

According to NOYB, Google makes ads appear in Gmail user’s inboxes that appear to be regular emails, which would be a direct violation of the EU’s ePrivacy directive, as folks may not have technically signed up or consented to see this stuff.

“When commercial emails are sent directly to users, they constitute direct marketing emails and are regulated under the ePrivacy directive,” NOYB said.

Because Google “successfully filters most external spam messages in a separate spam folder,” NOYB claims, when unsolicited messages end up in a user’s inbox it gives the impression it was something they actually signed up for, when that’s not the case.

“EU law already makes it quite clear: the use of email, for the purpose of direct marketing, requires user consent,” NOYB said, referencing an EU Court of Justice press release [PDF] from 2021 that outlines rules surrounding inbox advertising.

“It is quite simple. Spam is a commercial email sent without consent. And it is illegal. Spam does not become legal just because it is generated by the email provider,” said NOYB lawyer Romain Robert.

France’s Data Protection Authority (CNIL) has ruled in opposition to Google’s past behavior before. In February, Google was found to be breaching GDPR regulations by transmitting data to the US. Google has also been fined by the French Competition Authority for not paying French publishers when using their content.

NOYB said in its complaint [PDF] to CNIL that, because it accuses Google of violating the ePrivacy directive and not GDPR, the watchdog has no need to cooperate with, or wait for, the actions of other national data privacy authorities to decide to fine or otherwise penalize the American web giant.

Nobelium is back with a new post-compromise tool

Microsoft security researchers have described custom software being used by Nobelium, aka Cozy Bear aka the perpetrators of the SolarWinds attack, to maintain access to compromised Windows networks.

Dubbed MagicWeb by Redmond, this malicious Windows DLL, once installed by a high-privileged intruder on an Active Directory Federated Services (ADFS) server, can be used to ensure any user attempting to log in is accepted and authenticated. That’ll help attackers get back into a network if they somehow lose their initial access.

Microsoft noted that MagicWeb is similar to the FoggyWeb malware deployed in 2021, and added that “MagicWeb goes beyond the collection capabilities of FoggyWeb by facilitating covert access directly.”

This isn’t a theoretical malware sample, either: Microsoft said it found a real-world example of MagicWeb in action during an incident response investigation. According to Microsoft, the attacker had admin access to the ADFS system, and replaced a legitimate DLL with the MagicWeb DLL, “causing malware to be loaded by ADFS instead of the legitimate binary.”

MagicWeb is a post-compromise malware that requires the attacker to already have privileged access to their target’s Windows systems. Microsoft recommends treating ADFS servers as top tier assets and protecting them just like one would a domain controller.

Additionally, Microsoft recommends domain administrators enable Inventory Certificate Issuance policies in PKI environments, use verbose event logging, and look out for Event ID 501, which indicates a MagicWeb infection.

Redmond said organizations can also avoid a MagicWeb infection by keeping an eye out for executable files located in the Global Assembly Cache (GAC) or ADFS directories that haven’t been signed by Microsoft, and adding AD FS and GAC directories to auditing scans.

Anti-cheat software hijacked for killing AV

It turns out role-playing game Genshin Impact’s anti-cheat software can be, and is being, used by miscreants to kill antivirus on victims’ Windows computers before mass-deploying ransomware across a network.

TrendMicro said it spotted mhyprot2.sys, the kernel-mode anti-cheat driver used by Genshin, being used kinda like a rootkit by intruders to turn off end-point protection on machines. The software is designed to kill off unwanted processes, such as cheat programs.

You don’t have to have the game installed on your PC to be at risk, as ransomware slingers can drop a copy of the driver on victims’ computers and use it from there.

It has the privileges, code signing, and features needed by extortionists to make their roll out of ransomware a cinch, we’re told. TrendMicro recommends keeping a look out for unexpected installations of the mhyprot2 driver, which should show up in the Windows Event Log, among other steps detailed in the link above. ®

Safe Security has made available a free cybersecurity benchmarking tool for predicting cyberattack risk within vertical industry segments and can be tuned by organizations to better assess their own chances of being attacked.

Saket Modi, Safe Security CEO, said the CRQ Calculator combines cybersecurity threat intelligence and telemetry data it collects to ascertain attack costs with metadata collected from primary sources, such as reports published by the Securities and Exchange Commission (SEC) and insurance claims, that is accessible via application programming interfaces (APIs).

That data uses Bayes’ theorem to generate reports for specific vertical industries that determine, for example, that the probability of a health care company falling victim to a successful cyberattack is 25% compared to 20% for a financial services company. Industries such as manufacturing and retail face less than a 15% probability of a successful cyberattack.

The overall goal is to give organizations a better appreciation for the actual level of risk they face so they can make better cybersecurity investment decisions based on business context, noted Modi. That’s become more critical as a downturn in the overall global economy forces more organizations to reduce costs, he noted.

While there is a greater appreciation for cybersecurity than ever, many organizations are struggling to determine what level of spending is required to mitigate the threats they face. Before those assessments can be made there is a need to determine the actual level of threat to a vertical industry.

Spending on cybersecurity as a percentage of the overall IT budget has certainly increased in recent years. However, cybersecurity leaders are being asked more often to determine some level of return on investment (ROI) for that spending. Ultimately, the goal is to determine what level of spending makes sense based on what similar organizations are spending.

Of course, there is no correlation between spending and the level of cybersecurity attained. While the volume and sophistication of attacks have increased, most of the cybersecurity issues organizations encounter can be traced back to human error. Most organizations would dramatically improve their overall cybersecurity simply by focusing on fundamental processes that, in many cases, would eliminate the number of misconfigurations that cybercriminals can potentially exploit, for example.

At the same time, the number of attack surfaces that need to be defended continues to increase, so there does need to be some corresponding increase in cybersecurity. Most of the cyberattacks being launched are fairly rudimentary; cybercriminals don’t see the need to invest more time and effort when it’s relatively simple for them to compromise credentials and gain unfettered access to an IT environment.

Organizations can’t stop these attacks from being launched, but the hope is that by making it more difficult for cybercriminals to succeed they will concentrate their efforts elsewhere. Ultimately, if enough organizations improve their cybersecurity posture, the cost of launching attacks might one day become cost-prohibitive for attackers.

Unfortunately, organizations are a long way from achieving that goal. At the very least, organizations should have a better understanding of how much they need to spend on cybersecurity today as they look to continuously improve cybersecurity in the months and years ahead.

AXA’s branches in Thailand, Malaysia, Philippines and Hong Kong have been hit by a ransomware attack, with hackers claiming they have accessed more than 3-terabytes of sensitive data.

Included in that trove of data, according to the hackers, are customer medical reports – which is also said to expose their sexual health problems – as well as identification documents, bank account statements, payment records, contracts and details of individual claims.

In addition to the ransomware attack, AXA has also been hit by a series of distributed denial of service (DDos) attacks on its global websites that made the insurance giant’s website completely inaccessible for a number of hours.

A ransomware group by the name of Avaddon has taken responsibility for the ransomware attacks launched against AXA, just days after the company announced it would stop underwriting policies that included payouts in the event of a ransomware attack.

The group told AXA that the insurance giant has around 10 days to get in contact and meet their demands, otherwise risking the publication of massive amounts of sensitive information on their customers.

AXA has responded to the claims, telling Bleeping Computer that there is “no evidence” to suggest that data beyond one of its Thai operations was accessed.

“Asia Assistance was recently the victim of a targeted ransomware attack which impacted its IT operations in Thailand, Malaysia, Hong Kong and the Philippines.”

The insurer continued to explain that “a dedicated taskforce with external forensic experts is investigating the incident. Regulators and business partners have been informed.”

“As a result, certain data processed by Inter Partners Assistance (IPA) in Thailand has been accessed. At present, there is no evidence that any further data was accessed beyond IPA in Thailand.

“AXA takes data privacy very seriously and if IPA’s investigations confirm that sensitive data of any individuals have been affected, the necessary steps will be taken to notify and support all corporate clients and individuals impacted,” the company spokesperson said.

AXA is yet to address any specific demands of the hacking group Avaddon.

As Jack Jones, co-founder of RiskLens, tells the story, he started down the road to creating the FAIR™ model for cyber risk quantification because of “two questions and two lame answers.” As CISO at Nationwide insurance, he presented his pitch for cybersecurity investment and was asked:

“How much risk do we have?”

“How much less risk will we have if we spend the millions of dollars you’re asking for?”

To which Jack could only answer “Lots” and “Less.”

“If he had asked me to talk more about the ‘vulnerabilities’ we had or the threats we faced, I could have talked all day,” he recalled in the FAIR book, Measuring and Managing Information Risk.

In that moment, Jack saw the need for a way that cybersecurity teams could communicate risk to senior executives and boards of directors in the language of business, dollars and cents.

Some CISOs are still in the position of Jack pre-quantification – talking all day and delivering lame answers, from the board’s point of view. Here’s a short guide to what they’re not saying – and how RiskLens, the analytics platform built on FAIR, can provide the right answers.

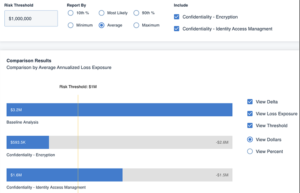

1. I don’t really know what our top risks are

I can ask a group of subject matter experts in the company to vote on a top risks list based on their opinions, but that’s as close as I can get.

Top Risks is the first report that many new RiskLens users run, and it only takes minutes, using the Rapid Risk Assessment capability of the RiskLens platform. The platform guides you through properly defining a set of risks (say, from your risk register) for quantitative analysis according to the FAIR standard. To speed the process, the platform draws on data from pre-populated loss tables. The resulting analysis quickly stack-ranks the risks for probable size of loss in dollar terms, across several parameters.

2. I can’t give you an ROI on the money you give me to invest in cybersecurity

You see, cybersecurity is different from other programs you’re asked to invest in – it’s constantly changing and never-ending. You never really hit a point of success; you just chip away at the problem.

With Top Risks in hand, RiskLens clients can dig deeper on individual scenarios and run a Detailed Analysis to expose the drivers of risk to see, for instance, what types of threat actors account for the highest frequency of attacks or what classes of assets account for the highest probable losses. Then they can run the Risk Treatment Analysis capability of the platform to evaluate controls for their ROI in risk reduction.

3. I can’t really tell you if things are getting better on cyber risk.

I can show you our progress with compliance checklists and maturity scales, and I hope you’ll assume that’s reducing risk.

While compliance with NIST CSF, CIS Controls, etc. is good and useful, these frameworks don’t measure performance outcomes in reducing risk – that takes a quantitative approach. The RiskLens platform can aggregate risk scenarios to generate risk assessment reports showing risk across the enterprise or by business unit, in dollar terms – and to show risk exposure over time. It’s easy to update and re-run risk assessments, thanks to the platform’s Data Helpers that store risk data for re-use. Update a Data Helper, and all the related risk scenarios update at the same time – and so do the aggregated risk assessments.

4. I can’t help you set a risk appetite.

I don’t really know how much risk we have and am pretty much operating on the principle that no risk is acceptable.

Boards should have a strong sense of their appetite for risk in cyber as in all fields, but qualitative (high-medium-low) cyber risk analysis only supports vague appetite statements that are difficult to follow in practice. On the RiskLens platform, a CISO can input a dollar figure for “risk threshold” as a hypothetical, and run the analyses to rank how the various risk scenarios stack up against that limit, making a risk appetite a practical target.

5. I don’t know how to align cyber risk management with the other forms of risk management we do.

Enterprise risk, operational risk, market risk, financial risk—I’ve heard their board presentations in quantitative terms. But cyber is just different.

Quantification is the answer – reporting on cyber risk in the same financial terms that the rest of enterprise risk management programs employ finally gives the board what it wants to hear on cyber risk management. ISACA, the National Association of Corporate Directors and the COSO ERM framework have all recommended FAIR for board reporting. As an ISACA white paper said,

The more a risk-management measurement resembles the financial statements and income projections that the board typically sees, the easier it is for board members to manage cybersecurity risk…FAIR can enable the economic representation of cybersecurity risk that is sorely missing in the boardroom, but can illuminate cybersecurity exposure.

If you hold any job related to security operations analysis and reporting, you’ve likely been inundated with news stories about data breaches and attacks by hackers on businesses of all sizes across numerous verticals. But with all that noise, it can be difficult to sort out the information that truly matters, like the hard data that helps you decide which solutions to adopt, gives you a powerful case to bring to your executive team for a larger cyber security budget next quarter, or simply reassures you that your peers are facing similar challenges.

For that reason, SwinLane.com have assembled some of the most impactful, telling statistics related to information security in one place

1. Cyber attacks cost businesses $400 billion every year—Lloyd’s of London, 2015

2. Some 42 percent of survey respondents said security education and awareness for new employees played a role in deterring a potential criminal. — “US cybercrime: Rising risks, reduced readiness; Key findings from the 2014 US State of Cybercrime Survey,” PwC

3. There are more than 1 million unfilled information security jobs globally; by 2017 that number may be as high as 2 million— “2014 Annual Security Report,” Cisco; UK Parliament Lords’ Digital Skills Committee witness interview

4. The malware used in the Sony hack would have slipped past 90 percent of defenses today. — Joseph Demarest, assistant director of the FBI’s cyber division, during a U.S. Senate hearing

5. The average U.S. business deals with 10,000 security alerts per day. — “State of Infections Report Q1 2014,” Damballa

6. A significant 90 percent of CISOs cite salary as the top barrier to proper staffing. — “State governments at risk: time to move forward,” Deloitte/NASCIO

7. About 43 percent of businesses experienced a data breach in 2014. — “Is Your Company Ready for a Big Data Breach? The Second Annual Study on Data Breach Preparedness,” Experian/Ponemon Institute

8. Just 21 percent of IT professionals are confident that their information security technologies can mitigate risk. — “2015 Vulnerability Study,” EiQ Networks

9. As many as 75 percent of breaches go undiscovered for weeks or months. — Michael Siegel, research scientist at MIT, at a recent cyber security conference

10. In an effort to combat the growing threat of cybercrime, the U.S. Department of Homeland Security increased its cyber security budget 500 percent during the past two years; and President Obama included $14 billion for cyber security spending in his 2016 budget. — GCN.com, 2015

What is most beneficial about cyber security safeguards, Well, you will not only benefit from the better protection of your own information, but you will also gain a competitive advantage by demonstrating your cyber credentials.

English: ISMS activities and their relationship with Risk Management (Photo credit: Wikipedia)

For example, certification to ISO 27001 or evidence of compliance with the PCI DSS (for merchants and service providers) is often a tender or contractual requirement because it proves that an organization has been independently audited against internationally recognized security standards.

Those that implement an information security management system (ISMS) will benefit hugely from improved processes and control of data within the organization.

Furthermore, improving and having demonstrable cyber security can also reduce your cyber security insurance. And finally, it will also dramatically reduce the chances of you experiencing a cyber attack. That’s kind of improvement.

October is National Cyber Security Awareness Month and it is an opportunity to engage public and private sector stakeholders – especially the general public – to create a safe, secure, and resilient cyber environment. Everyone has to play a role in cybersecurity. Constantly evolving cyber threats require the engagement of the entire nation — from government and law enforcement to the private sector and most importantly, the public.

A cyber security risk assessment is necessary to identify the gaps in your organisation’s critical risk areas and determine actions to close those gaps. It will also ensure that you invest time and money in the right areas and do not waste resources where there is no need for it.

Even if you have implemented an ISO 27001 Information Security Management System, you may want to check if your cyber security hygiene is up to standard with the industry guidelines.

Use an in house qualified staff or an experienced consultant(s), who will work with your team to examine each of the ten risk areas (described below) in sufficient detail to identify strengths and weaknesses of your current security posture. All this information can be consolidated and immediately usable action remediation plan that will help you close the gap between what you are actually doing and recognized good practice. It will enable you to ensure that your cyber risk management at least matches minimum industry guidelines.

Do you have an effective risk governance structure, in which your risk appetite and selected controls are aligned? Do you have appropriate information risk policies and adequate cyber insurance?

Do you have a mobile and home-working policy that staff have been trained to follow? Do you have a secure baseline device build in place? Are you protecting data both in transit and at rest?

Do you have Acceptable Use policies covering staff use of systems and equipment? Do you have a relevant staff training programme? Do you have a method of maintaining user awareness of cyber risks?

Do you have clear account management processes, with a strong password policy and a limited number of privileged accounts? Do you monitor user activity, and control access to activity and audit logs?

Do you have a policy controlling mobile and removable computer media? Are all sensitive devices appropriately encrypted? Do you scan for malware before allowing connections to your systems?

Do you have a monitoring strategy? Do you continuously monitor activity on ICT systems and networks, including for rogue wireless access points? Do you analyze network logs in real time, looking for evidence of mounting attacks? Do you continuously scan for new technical vulnerabilities?

Do you have a technical vulnerability patching program in place and is it up-to-date? Do you maintain a secure configuration for all ICT devices? Do you have an asset inventory of authorized devices and do you have a defined baseline build for all devices?

Do you have an appropriate anti-malware policy and practices that are effective against likely threats? Do you continuously scan the network and attachments for malware?

Do you protect your networks against internal and external attacks with firewalls and penetration testing? Do you filter out unauthorised or malicious content? Do you monitor and test security controls?

Do you have an incident response and disaster recovery plan? Is it tested for readily identifiable compromise scenarios? Do you have an incident forensic capability and do you know how to report cyber incidents?

Cyber wars between companies, hacker groups and governments can force entire countries to a standstill. A lone, but sophisticated, hacker can bring global organisations to their knees from just an internet café. The threat isn’t even entirely external; perhaps the greatest threat sits uncomfortably in plain sight – from inside your staff. Arm yourself with the top cyber security titles:

This book is written by Dr Julie Mehan who is a Principal Analyst for a strategic consulting firm in the State of Virginia. She has been a Government Service employee, a strategic consultant, and an entrepreneur – which either demonstrates her flexibility or inability to hold on to a steady job! Until November 2007, she was the co-founder of a small woman-owned company focusing on secure, assured software modernization and security services. She led business operations, as well as the information technology governance and information assurance-related services, including certification and accreditation, systems security engineering process improvement, and information assurance strategic planning and programme management. During previous years, Dr Mehan delivered information assurance and security-related privacy services to senior department of defence, federal government, and commercial clients working in Italy, Australia, Canada, Belgium, and the United States.

The world is becoming ever more interconnected and vulnerable, as has been demonstrated by the recent cyber attacks on Estonia. Thus the need for stringent and comprehensive methods for combating cyber crime and terror have never before been need more than now.

Information security should not be an after thought. It should be ingrained into the organisation’s culture. This book will help you create this forward thinking culture using best practices and standards. Key Features:

Straightforward and no-nonsense guide to using best practices and standards, such as ISO 27001, to instil a culture of information security awareness within an organisation.

Distils key points on how to use best practices and standards to combat cyber crime and terror.

The information within the book is presented in a straightforward and no-nonsense style, leading the reader step-by-step through the key points.

What other people say about this book:

So what you have in CyberWar, CyberTerror, CyberCrime is a skillful blend of very readable, at times even entertaining and certain to stimulate introspection, guidance on just why and how cyber security is important to every organization connected to the internet – try to name one that is not . I would bet that truly effective leaders will purchase multiple copies and circulate CyberWar, CyberTerror, CyberCrime throughout the entire organization. Leonard Zuga, Partner, Technology and Business Insider (TBI)

“This book is a good basis for a security roadmap. It’s well researched and well written.”

Peter Wood, Chief of Operations at First Base Technologies

“This is a book that I will look forward to using to enhance both my undergraduate and graduate instruction in information security.”

Dr Bob Folden, Assistant Professor, Business Administration and MIS, Texas A&M University – Commerce

“This is an interesting book that introduces the reader to the security of the Internet industry, goes into some details on how some abuse it. This is a very good book. You will enjoy it.”